The most seductive category — and the most overlapping with your all-world core. Before adding any tech satellite, check how much of it already sits in FWRA/VWRA at full market-cap weight.

BOTZ

FROZEN · NOT ADDING

Global X Robotics & AI ETF · US-listed · 0.68% TER

Additive to FWRA? Partial — Japanese industrials are additive; Nvidia is already in your core

About 50 companies at the intersection of robotics and artificial intelligence. Unique mix: ~50% US names (Nvidia, Intuitive Surgical) + ~25% Japanese industrials (Keyence, Fanuc, Yaskawa). Not a pure US-tech bet — the Japanese industrial layer is genuinely exposure the all-world core underweights.

The case for it

- Genuinely additive: Japanese robotics names (Keyence, Fanuc) are at fractions of a percent in the all-world core

- Structural demand: ageing populations, labour shortages, reshoring — real, non-cyclical tailwinds

- Humanoid robotics now a formal sub-theme — theme getting broader, not narrower

- Quadrupling global robotics market forecast over next decade (multiple analyst sources)

The case against it

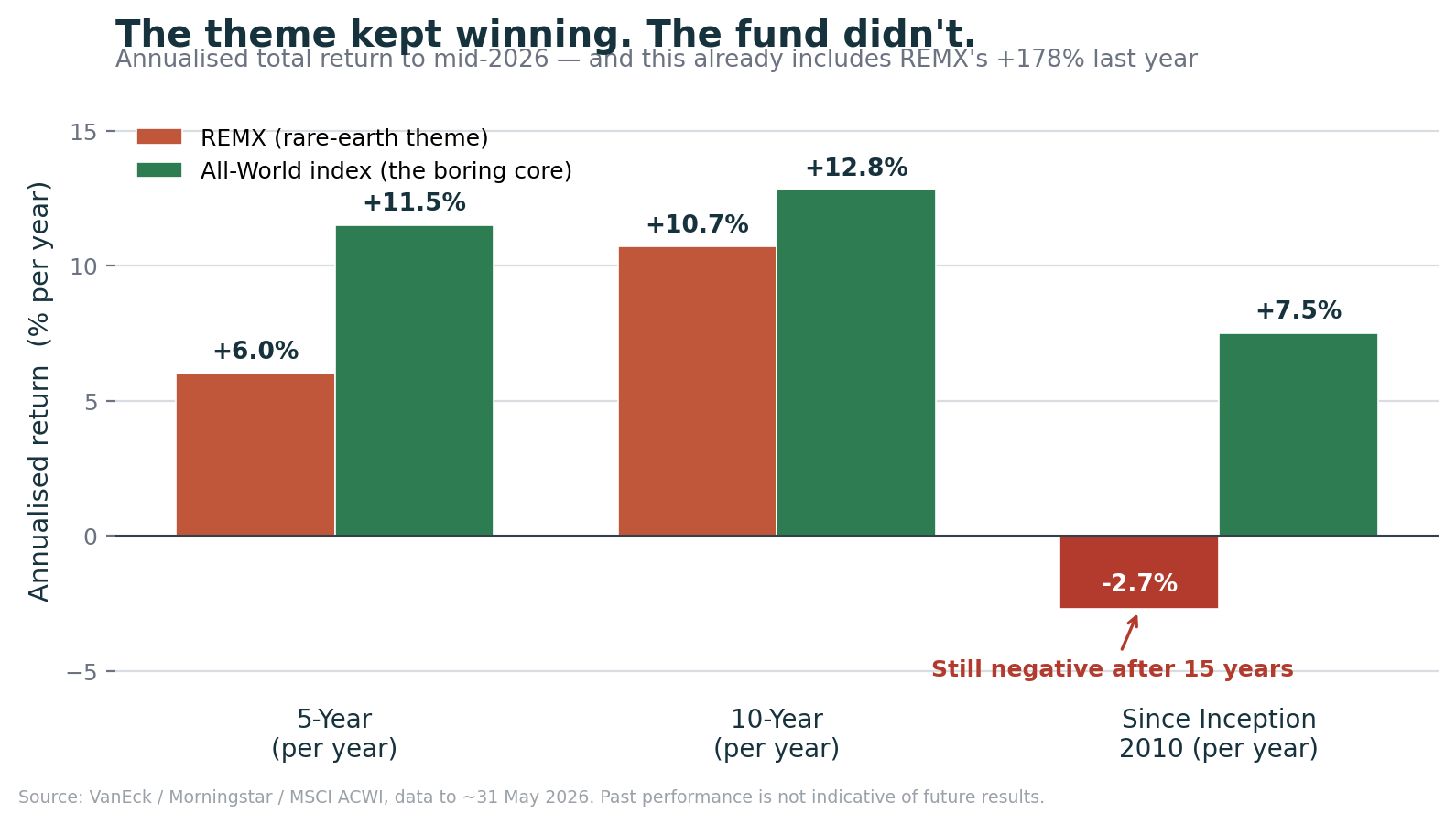

- 5-year annualised return: +0.03% — basically flat through the entire AI/robotics boom

- Timing risk: bought into an already-popular theme at peak valuation

- US-listed: 30% dividend WHT (yield ≈ −0.09%, fee ate the dividend before tax could)

- 0.68% TER = 4.5× the cost of FWRA/year

- Fresh Start Test = no: would not buy fresh at this price and structure

My position

I was right about robots. The theme is real. It still barely mattered. Five years of the most exciting industrial story on earth, and the fund went sideways — because I bought the future at a price that already assumed it had arrived. The position is now frozen: too small to justify the flat trading fee to sell, too honest to pretend I'd add more. It lives in my account as a reminder — not of being wrong, but of the gap between a real theme and a good entry.

Quick reference — BOTZ

| Index tracked | Indxx Global Robotics & Artificial Intelligence Thematic Index |

| Domicile | United States (US-listed) |

| Holdings | ~50 stocks, non-diversified |

| TER | 0.68% / yr |

| Dividend yield | ≈ negative (fee eats it) |

| Worst drawdown | Significant — plan for −50%+ |

| Performance (5-yr p.a.) | +0.03% (to Mar 2026) |

| US estate tax? | Yes — US asset |

PNQI

KEPT · WITH RULES

Invesco Nasdaq Internet ETF · US-listed · 0.60% TER

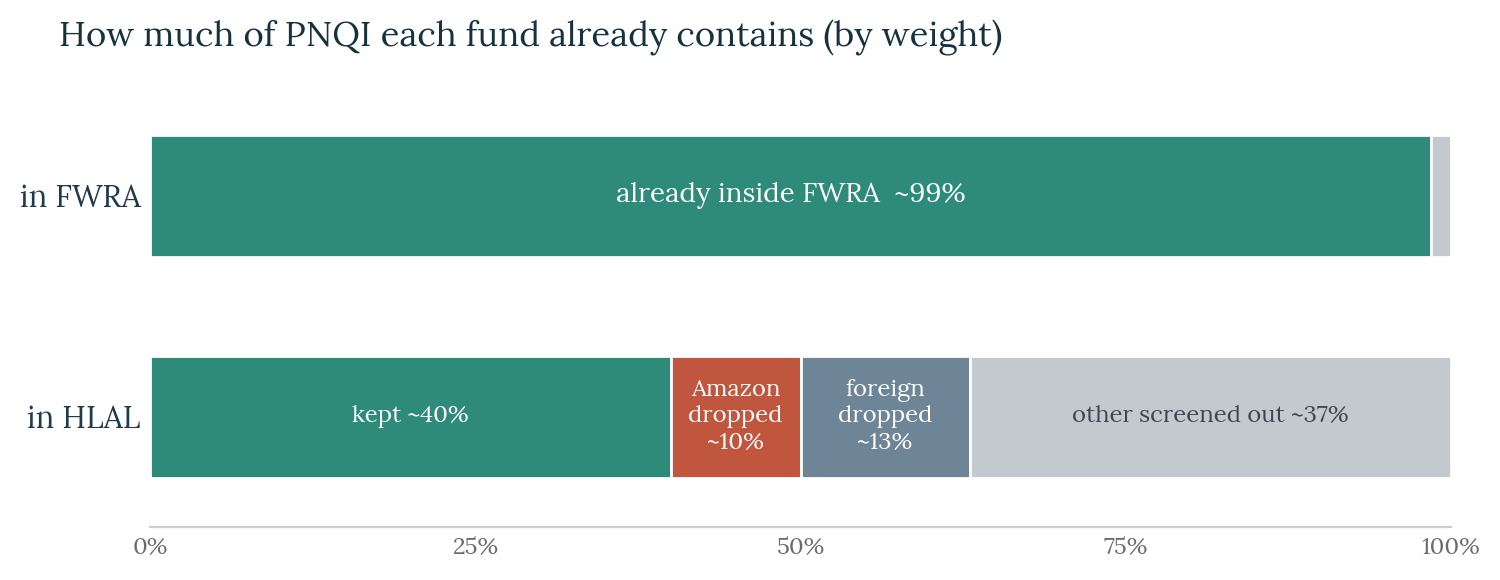

Additive to FWRA? ~99% already in FWRA — near-pure duplication

About 79 companies that earn their money from the internet: search, social media, e-commerce, streaming, cloud, online ads. Top 5 — Alphabet, Amazon, Apple, Microsoft, Meta — make up about 44% of the fund combined.

The case for it

- The internet theme is genuinely structural — it reshaped commerce, media, and enterprise permanently

- More internet-concentrated than a broad Nasdaq — different profile from the all-world core in terms of intent

- Dividend yield ≈ zero → 30% WHT barely bites (growth companies reinvest, not pay out)

- Running since 2008 — long track record

The case against it

- ~99% of PNQI by weight already sits inside FWRA — almost pure duplication, not diversification

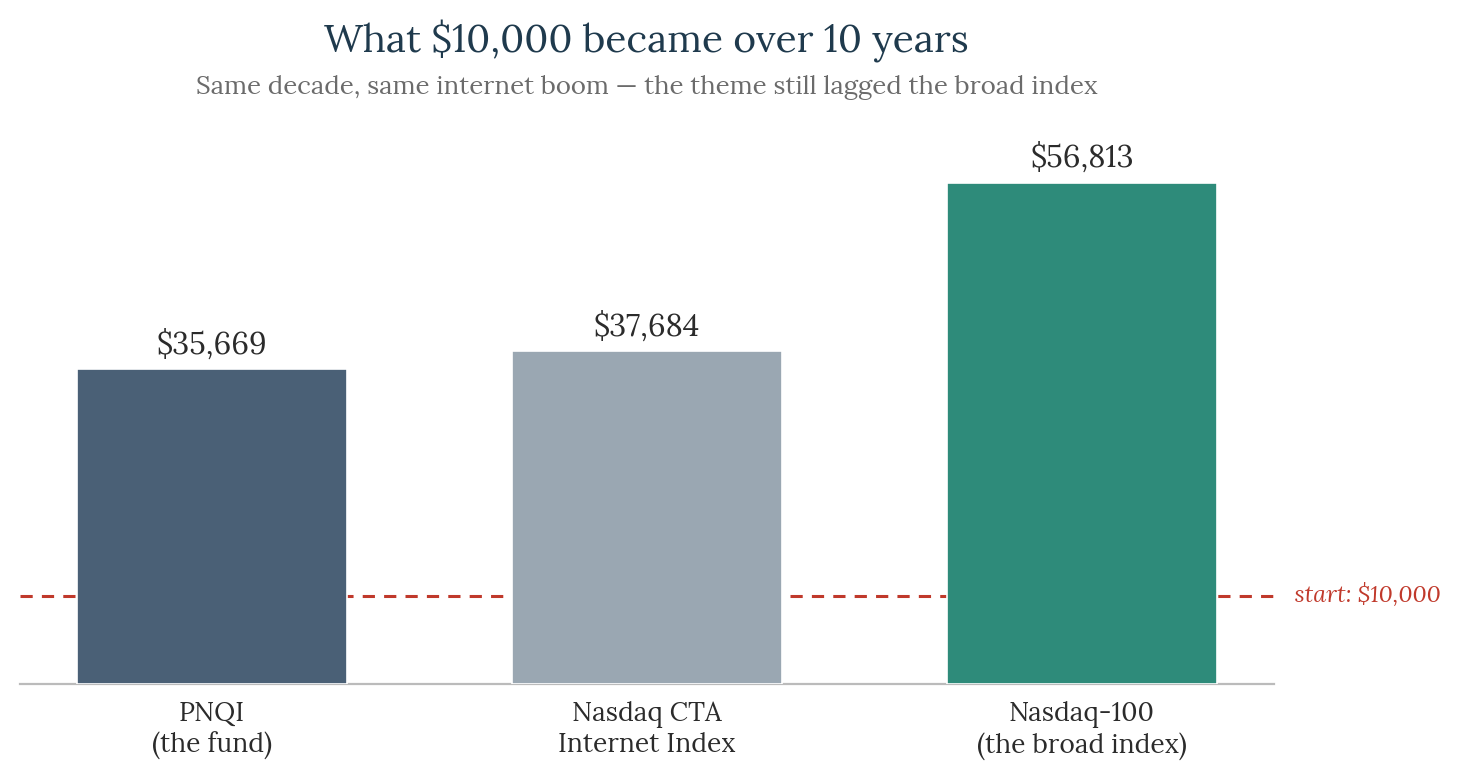

- 10-year performance: $10k → $35,669 vs plain Nasdaq-100 → $56,813 — theme lagged the broad index

- Even lagged its own index ($37,684) — 0.60% fee plus tracking friction

- 4× the cost of FWRA for a fund you almost entirely already own

- US-domiciled: US estate-tax exposure; no accumulating wrapper

My position

The most overlapping satellite I hold — and I kept it knowing that. It passes the Fresh Start Test only as a small, fenced, surplus-funded side bet; it fails immediately as a core. I kept it because I can afford to be wrong about it, and "I can afford to be wrong" is the only honest framing a fund like this deserves. It is on a review date, and it's judged against the Nasdaq-100, not against zero. The overlap number (~99% in FWRA) was the most uncomfortable thing I found when I actually checked.

Quick reference — PNQI

| Index | Nasdaq CTA Internet Index |

| Holdings | ~79 stocks |

| Domicile | United States |

| TER | 0.60% / yr |

| Overlap with FWRA | ~99% by weight |

| Overlap with HLAL (Shariah) | ~40% (Amazon screened out, foreign names excluded) |

| 10-yr return (own fund) | $10k → ~$35,669 |

| 10-yr return (Nasdaq-100) | $10k → ~$56,813 |

BUG

KEPT · BUSINESS PROFITS ONLY

Global X Cybersecurity ETF · UCITS (London) or US-listed · 0.50% TER

Additive to FWRA? Partial — platform leaders already in FWRA; smaller names are new exposure

Two versions, not the same fund. The US-listed BUG (NASDAQ) tracks Indxx Cybersecurity. The UCITS version (London: BUG LN, IE00BMH5Y871) tracks Indxx Cybersecurity v2 — ~30 stocks vs ~25, accumulating, no US estate-tax exposure. The UCITS version is recommended for long-term Malaysian holders even though the usual dividend-tax advantage barely applies here (near-zero yield).

About 30 cybersecurity software companies: Fortinet, Okta, Palo Alto, CrowdStrike, Akamai, Zscaler. ~87% United States, ~6% Israel. This is almost entirely an American software bet. Launched November 2021 — near the peak of the speculative tech bubble.

The case for it

- Non-discretionary spending — companies cannot stop defending themselves even in a recession; attackers don't take economic downturns off

- Permanently expanding attack surface: every new device, cloud workload and AI system is another door to lock

- AI helps attackers — the same customers buy more defence. Both sides of the arms race feed the same budget

- Market consolidation: fragmented point-solution vendors losing budget to platform giants inside this index

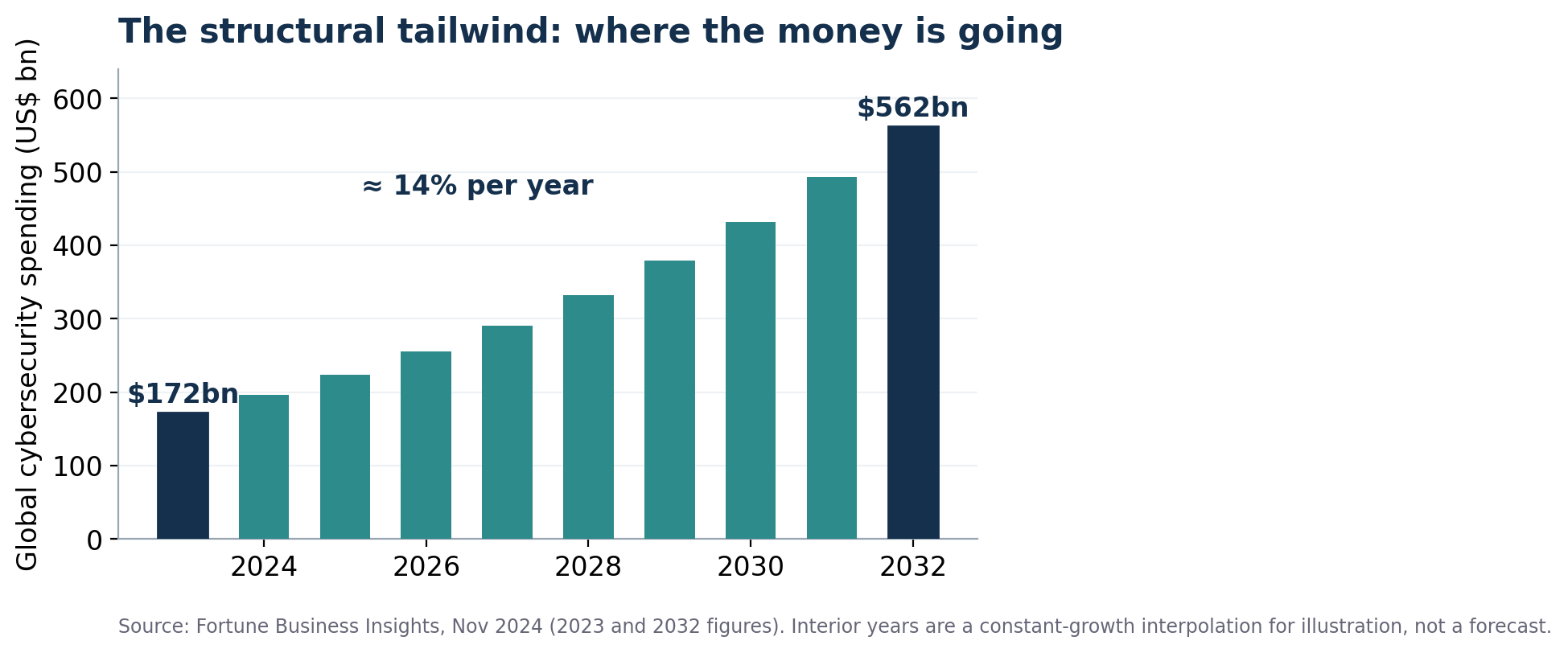

- Global spending forecast: ~$172bn (2023) → $562bn (2032), ~14%/yr structural growth

The case against it

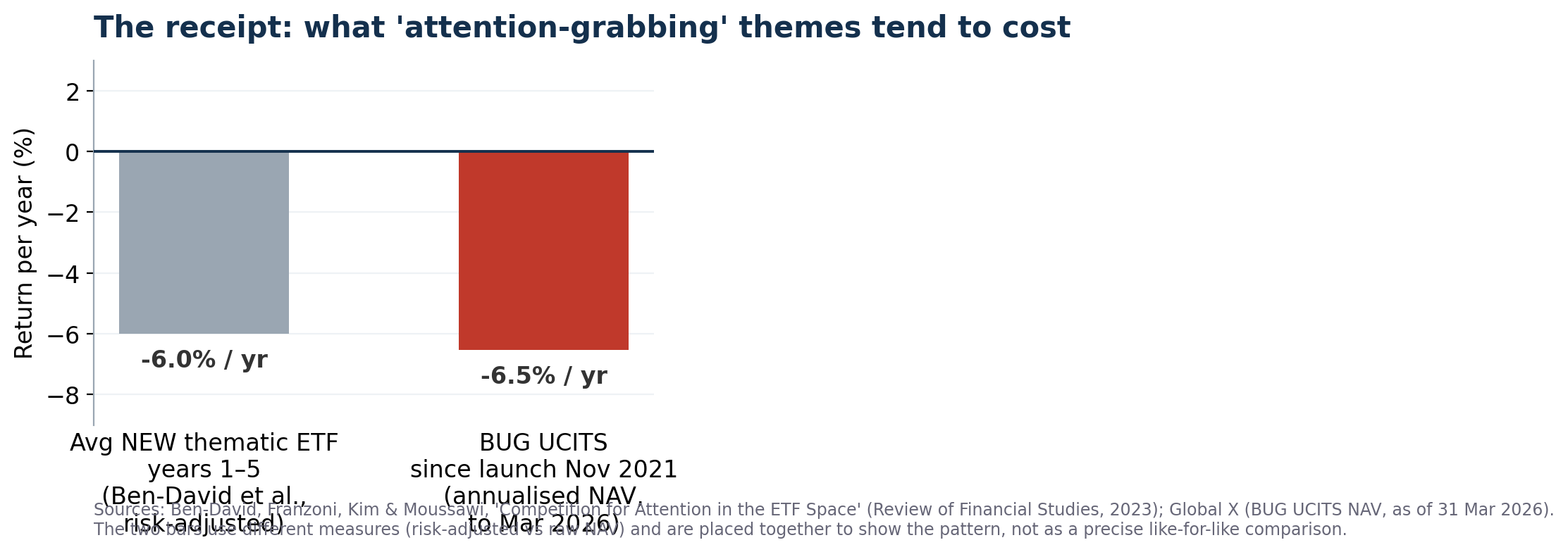

- Launched November 2021 — near the speculative tech peak. Since launch: −6.5%/yr annualised (to Mar 2026)

- Ben-David et al. (RFS 2023): thematic ETFs lose ~6%/yr risk-adjusted over first 5 years — BUG matches the academic average precisely

- Biggest names (Palo Alto, CrowdStrike, Fortinet) already sit inside FWRA — adding BUG doubles the leaders, adds a volatile second tier

- ~30 stocks, non-diversified, essentially 100% software — single bad earnings season for 2–3 names moves the whole fund

- UCITS version: only ~$63m AUM, 2021 launch — thin and new, closure risk exists

- 0.50% TER = 3× FWRA on a satellite that has lost money since launch

My position

Cybersecurity is one of the few themes with a structural enough demand story to justify a small satellite. Non-discretionary spending plus an attack surface that only grows is a better foundation than most themes. But the receipts are honest: launched at the peak, down since, matching exactly what the academic research predicts for attention-grabbing thematic funds. I hold the UCITS version, funded only from business profits, never core savings. Sized so that going to zero is a footnote, not a chapter.

Quick reference — BUG (both versions)

| BUG (US-listed) | BUG UCITS (recommended) |

|---|

| Listing | NASDAQ | London Stock Exchange (BUG LN) |

| ISIN | US37954Y3844 | IE00BMH5Y871 |

| Dividends | Distributing | Accumulating |

| US div. WHT | 30% | 15% (barely bites — yield ≈ 0.03–0.1%) |

| US estate tax | Yes | No |

| TER | 0.50–0.51% | 0.50% |

| AUM | ~US$0.9–1.2B | ~US$63M (tiny) |

| Since launch (annualised) | −6.5%/yr (Nov 2021 to Mar 2026) |

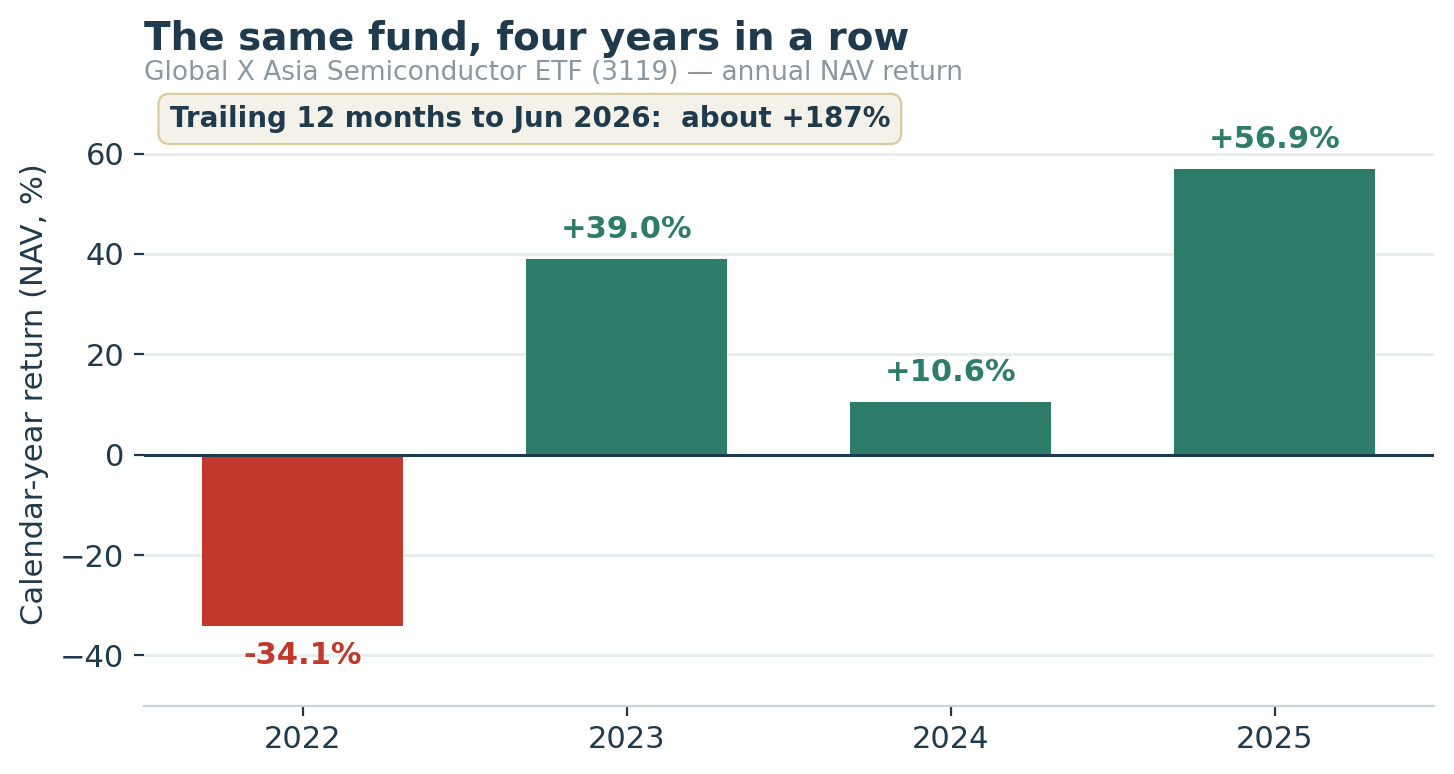

3119

KEPT · CONVICTION

Global X Asia Semiconductor ETF · HK-listed · 0.68% TER

Additive to FWRA? Yes — a genuinely additive Asia manufacturing layer

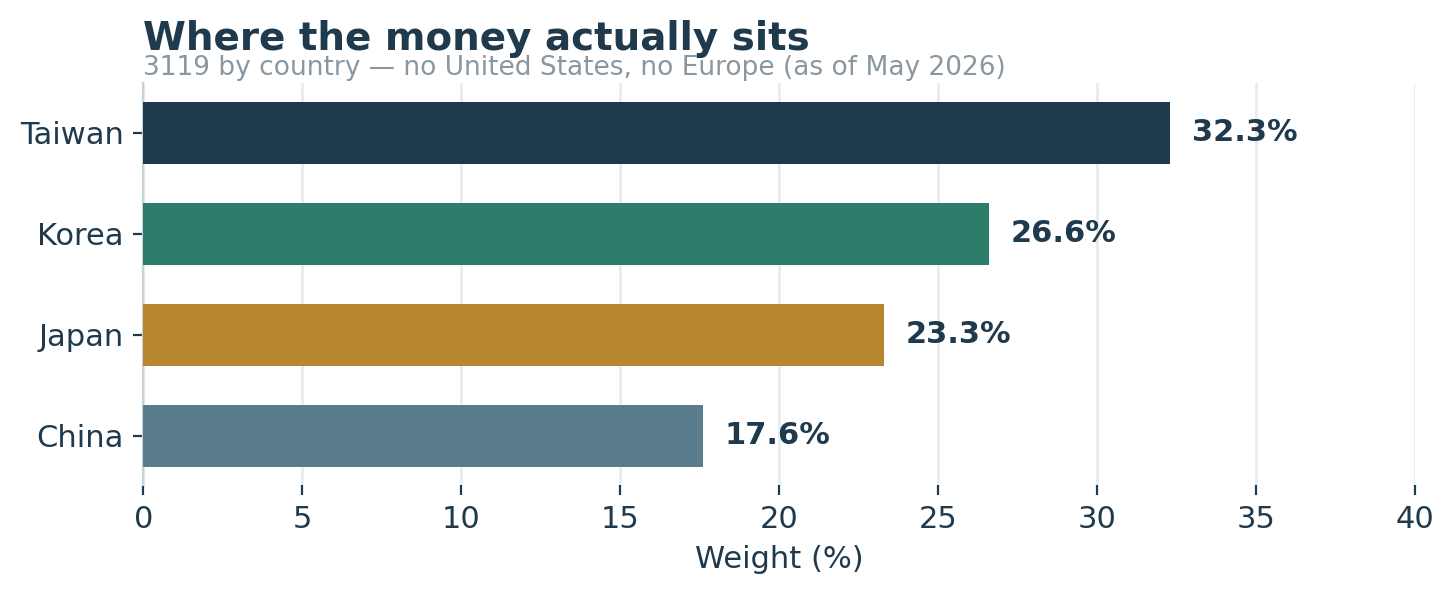

About 40 Asian companies that build chips rather than just design them: TSMC (foundry), Samsung and SK Hynix (memory), Tokyo Electron and Advantest (chip equipment), plus China's SMIC and Cambricon. Taiwan 32%, Korea 27%, Japan 23%, China 18%. No US. No Europe. This is the manufacturing end of the chip industry — the toll booths, not the cars.

The case for it

- Genuinely additive, not duplicate. TSMC and Samsung sit in FWRA at ~1% weight each. SK Hynix, MediaTek, Tokyo Electron, Advantest — the manufacturing layer — are essentially absent from the all-world core at meaningful weight

- Asia controls ~75% of world chip-making capacity; TSMC alone makes 70%+ of advanced chips

- AI memory bottleneck (HBM chips) is a two-horse race between SK Hynix and Samsung — both inside 3119

- Passes the overlap test: unlike CNDX, this is additive exposure, not a costume on what you already own

- Four regional sub-bets that don't move in lockstep: Korean memory, Taiwanese foundries, Japanese equipment, Chinese substitution

The case against it

- 91% one sector, top 10 = ~65% of the fund. A chip winter hits everything at once; nowhere to hide

- −34% in 2022 — a single calendar year. Chip cycles are brutal and repetitive

- +187% trailing 12 months to Jun 2026 — came after the recovery. Entry now is expensive

- 0.68% TER = 4.5× the core every year

- HK-domiciled, RMB underneath — the Ireland vs US WHT logic does not apply. Tax rules are different; verify with FSMOne directly

- Small fund (~HK$1.1B); index was just changed in mid-2026 — worth monitoring what you own

- Note: fund rules allow up to 50% in derivatives (currently physical, but permission exists)

My position

The satellite I feel most confident about. The Asian manufacturing layer — TSMC's moat, SK Hynix's HBM monopoly, Tokyo Electron's equipment stranglehold — is a genuinely different engine from what my all-world core owns. 3119 survived the cleanup when SMH didn't because it's additive. But after +187% in a year, I am not adding — I'm watching. The Fresh Start Test for a new entry is now a harder yes than it was 18 months ago.

Quick reference — 3119

| Full name | Global X Asia Semiconductor ETF |

| Exchange | Hong Kong Stock Exchange (FSMOne: 3119) |

| Holdings | 40 stocks · top 10 ≈ 65% |

| TER | 0.68% / yr |

| Countries | Taiwan 32% · Korea 27% · Japan 23% · China 18% |

| Domicile / currency | Hong Kong · HKD / RMB |

| Worst year on record | −34% (2022) |

| Trailing 12-month (to Jun 2026) | ~+187% |

| Fund size | ~HK$1.1B (relatively small) |